Market Report: Markets steady

Oct 14, 2016·Alasdair Macleod

Gold and silver had their big fall the previous week, so this week was one of consolidation with prices moving sideways.

Gold closed last Friday at $1258, and in early European trade today was more or less unchanged at $1256. Silver closed last Friday at $17.55, and in early European trade this morning was $17.48. Comex volume all week has been very subdued, and it has been as exciting as watching paint dry.

On Comex, gold’s open interest has now fallen a long way, from a high of 657,776 contracts on 11 July, to a current level of 495,457. This represents a destruction of a little over 500 tonnes of paper gold, worth $20.4bn. It is a substantial number obviously, and brings open interest down to the approximate levels that pertained at the end of May. Since that time, longer-term investors have become net buyers of gold in ETF form, and are also maintaining rolling long positions in the futures markets. It is therefore possible to conclude that even though open interest is close to its long-term average, the futures market is actually oversold. This is shown in our next chart.

It is interesting how open interest and the price are correlating tightly. If some contracts described as speculator’s interest actually represent managed investment exposure, gold could be finding a bottom around current levels.

Things behind the scenes are becoming potentially volatile, so this period of calm could come to an end in the next week or two. The dollar is enjoying a purple patch, driving the whole commodity complex into a consolidation phase. The dollar’s strength has also happened at a bad time for sterling, which is vulnerable to post-Brexit blues.

Sterling’s weakness is sure to make analysts begin to think about price inflation next year, and the wisdom of the bank cutting interest rates post-Brexit will therefore be questioned. In this week’s Insight article I point out the near-certainty of stagflation for sterling, which is likely to force the Bank of England to raise interest rates to support sterling. This could happen at any time, should sterling fall further.

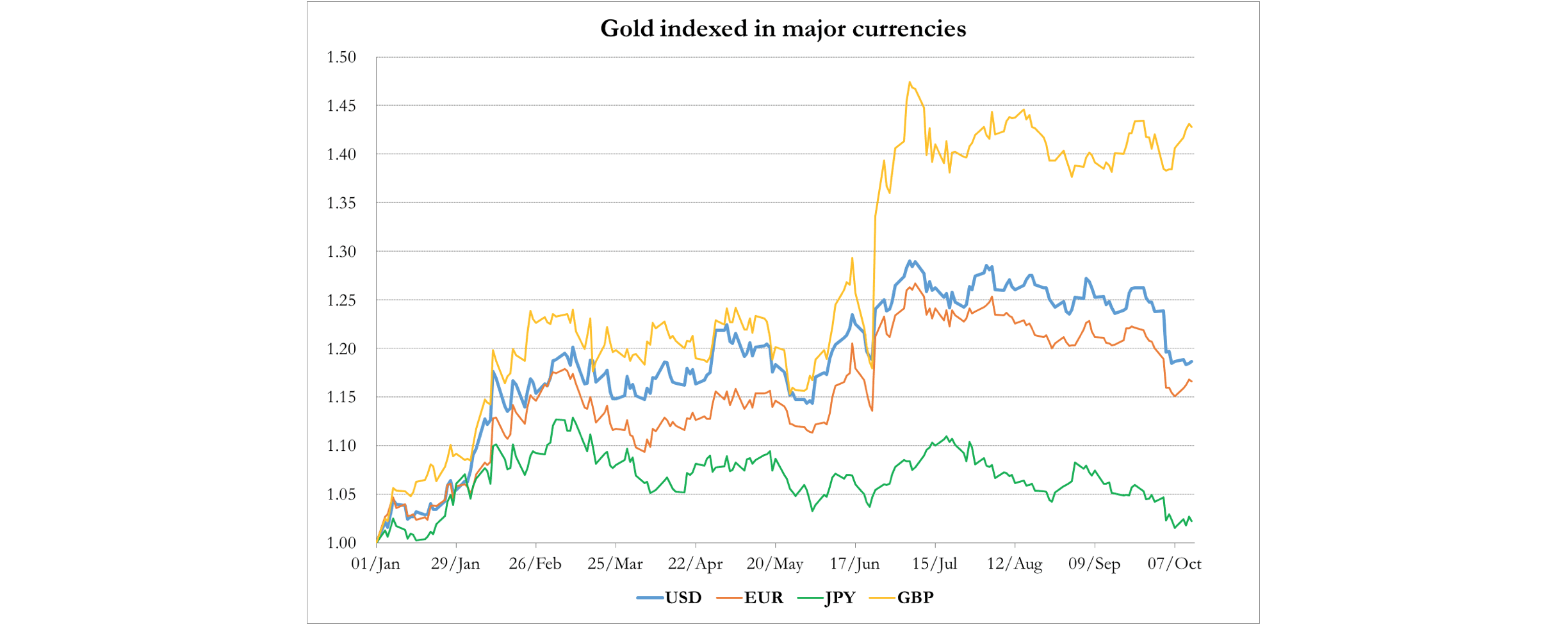

Sterling’s fall is in addition to the earlier improvement in producer prices for commodities and raw materials measured in pounds, which in the last fifteen months has reversed a fall of about 25% to a rise of the same degree. This represents a 50% turnaround in this measure of price inflation, which clearly indicates that consumer price inflation pressures in the UK will become the dominant issue next year. The dollar faces similar pressures, but to a lesser extent, with the dollar being less weak than sterling. Sterling’s woes are reflected in the next chart, which shows how it has fared against gold.

At one extreme, there is the yen, where the gold price has risen by a net 2% this year, and at the other, sterling, where the gold price is up 43%. So while traders look at gold as a buy or sell, ordinary people in Britain with some gold in their asset mix have seen gold do precisely what it should, and that is protect their purchasing power.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.