Market Report: Support at last December’s lows

Jul 6, 2018·Alasdair Macleod

Gold and silver have now given up all the promising gains of earlier in the year, and gold optimists will be hoping the buyers that bought so strongly last December will take the opportunity of these same levels to buy again. That is what forms the technical analysts’ bullish double-bottom formation.

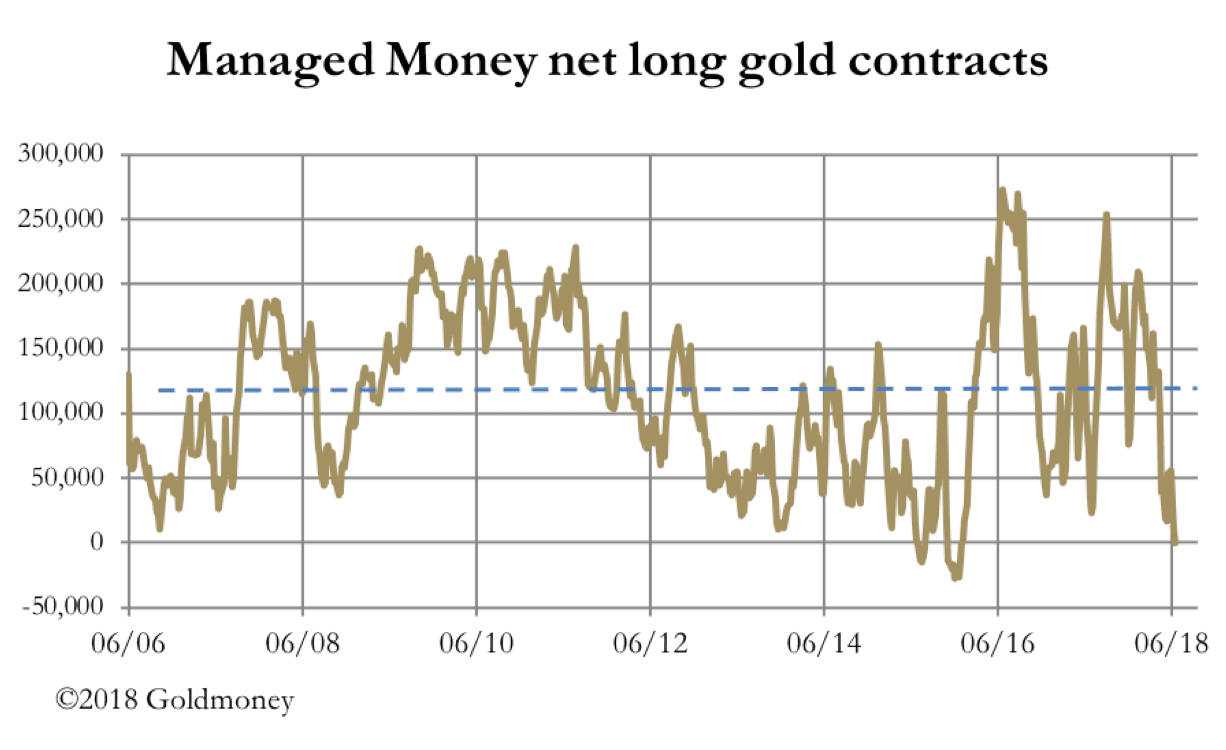

Supporting the case for a rally from here is the heavily oversold Comex position, with the hedge funds unusually net short as of the last Commitment of Traders report, which was for 26th June (an update for last Tuesday will be released after hours tonight). This is shown in our next chart.

The only times gold has been more oversold for major speculators were July 2015 and December 2015, which marked the end of the major bear market. This lends strong support to the double-bottom theory.

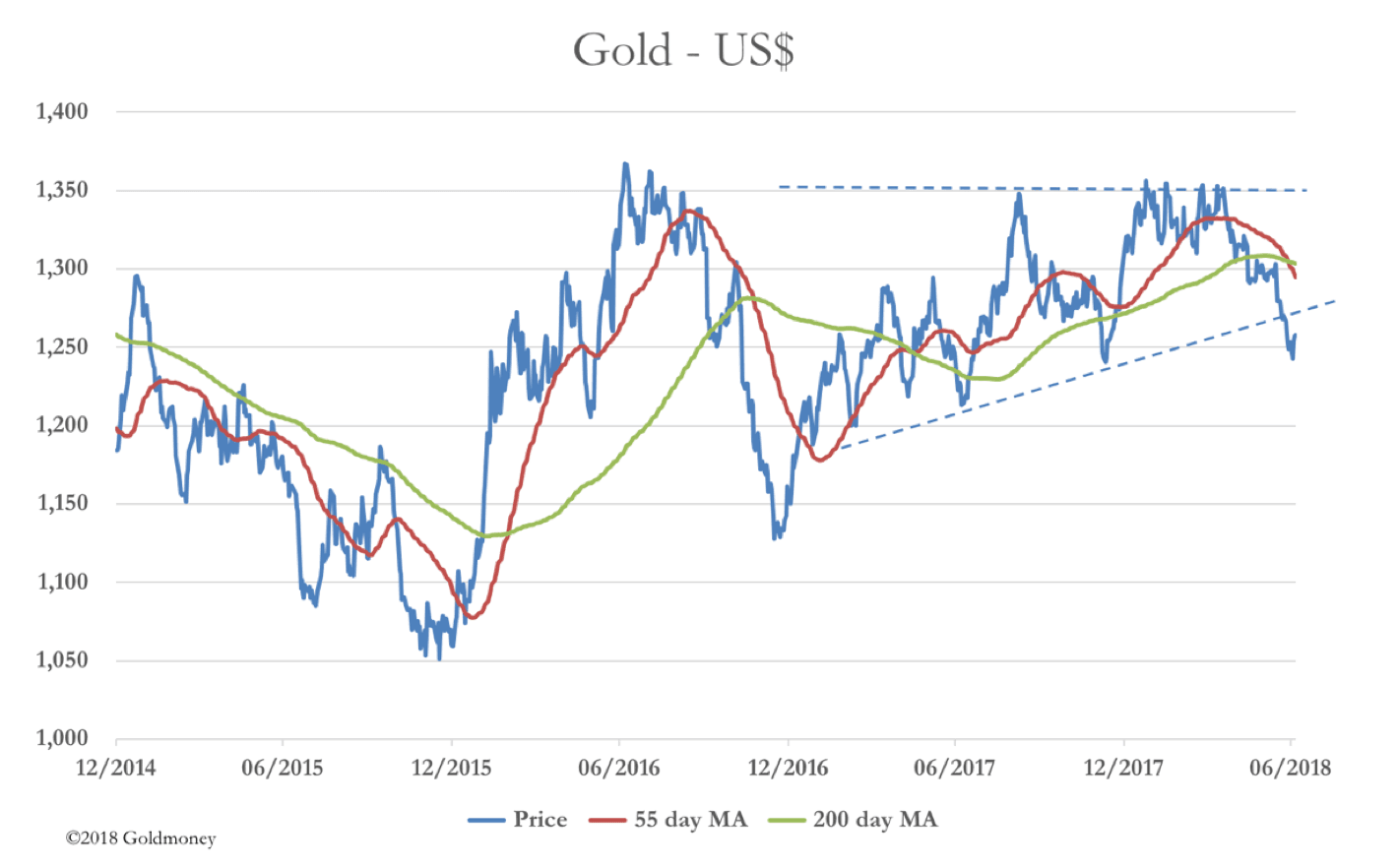

However, there is significant technical damage to repair, as our next chart shows.

The most negative feature of this chart is the death cross, which has the 55-day moving average falling beneath the 200-day, and these averages and the price all falling in bearish sequence. At a minimum, technical analysts will want to see the gold price back above $1300 and looking like mounting a challenge to the $1350 level. That seems a long way from here, particularly given that a break below $1240 would negate the double bottom theory.

So much for the technical position. In the real world, the US Fed realises the economy is growing robustly, but it sees evidence of business investment being deferred by uncertainties over trade tariffs. This might encourage the FOMC to edge towards moderation with regard to future interest rate increases until trade uncertainties resolve themselves.

Today, the US imposed new tariffs on $34bn of imports from China, with threats to extend them to all imported Chinese goods. While cautioning that the extension of tariffs is for the moment a negotiating position, it must be recognised tariffs are a tax on production and consumption. Tariffs will therefore increase price inflation. Furthermore, the price of oil is rising, despite President Trump jawboning the Saudis to increase output. Price inflation pressures are definitely mounting, and May’s CPI-U at 2.8% is already well above the target rate of 2%.

With business investment softening and M2 monetary growth stalling (4.6%) the Fed faces the unpleasant prospect of having to raise rates to curb price increases while a mild recession looks increasingly possible.

It is a common misconception that higher nominal interest rates are bad for the gold price. What matters is the inflation outlook and the monetary authorities response to it. If the Fed appears boxed in by rising prices and a softening economy, these will be the ideal conditions for a bull market in gold.

The key will be to watch both energy prices and developments over trade tariffs.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.