Precious metals round-up

Oct 24, 2019·Alasdair MacleodGrowing evidence of an economic downturn despite unprecedented monetary inflation since Lehman means a new credit and systemic crisis is becoming increasingly certain. In an attempt to prevent a new crisis developing, this time the scale of monetary inflation by the authorities will have to be even greater. The rise in the price of gold since December 2015 and its break-out from a three-year consolidation period earlier this year confirms that the risks of a credit and systemic crisis undermining fiat currencies have been increasing for some time.

It is now likely that in future portfolio managers will increase their investment allocations in favour of gold and actively consider investing in silver and platinum as well. It is in this context that this article looks at the price relationships between the three precious metals and their relevant monetary and investment characteristics.

Introduction

Markets are playing a dangerous game of chicken with economic reality, which every passing day tells us that trade is slowing, and credit everywhere is maxed out. Key economies are beginning to reflect this in statistics, having for much of this year screamed the message at us through business surveys. Central banks know their monetary policies have failed. The ECB has already announced deeper negative deposit rates and is reviving its asset purchase programme (printing) from next month. The Fed is injecting liquidity (more printing) through repos in far larger quantities into its monetary system which, mysteriously, is short of money despite commercial banks having combined reserves of $1.44 trillion at the Fed.

We should not be surprised at its inability to join the dots between cause and effect, but warnings from the IMF about a $19 trillion corporate debt timebomb, coming from an organisation that is the deep-state of the economic system and has been consistently advocating monetary inflation, is tantamount to an official admission of global monetary failure. Where to now? Print, and print again.

Meanwhile, government bond yields and even some corporate ones are in negative territory. The only respectable government bonds that are not are US Treasuries and UK gilts, but in real terms arguably they are already there. Equity markets are within a whisker of all-time highs. The collective hype is a belief that a new round of increasingly aggressive printing will buy off an economic slump, but it is a rotten logic born out of economic ignorance and desperation.

It is like a game of chicken: investors riding a Vespa scooter flat out in the middle of the highway, facing the oncoming juggernaut of reality from the opposite direction. We know what the result will be, because we have seen it before. And we know who gets killed.

This article is not aimed at those riding the Vespa: being committed to do or die they are in a mental zone from which logic is excluded. It is for those who know or suspect that the monetary and economic situation is serious and getting more so by the day. It is for those who know why an accelerating debasement of fiat currencies is now inevitable.

Not only have we been warned of the economic dangers by the IMF, the Bank for International Settlements and everyone else in authority, but a global banking system with fatal weak points is plain to see. Even McKinsey, consultants favoured and listened to by governments everywhere, in their global banking annual review says it’s all late cycle. They write,

“…on balance, the global banking industry approaches the end of the cycle in less than ideal health with nearly 60% of banks printing returns below the cost of equity. A prolonged economic slowdown with low or even negative interest rates could wreak further havoc.”[i]

We should pause to think about it. This bastion of the establishment is confirming that a systemic collapse is becoming more certain by the day.

Germany, until now by far the best-performing economy in the Eurozone, faces the prospect of having to support its major banks, one of which (Deutsche Bank) has positions in derivatives amounting to an estimated €45 trillion, nearly twelve times Germany’s GDP. Deutsche Bank has a much-reduced balance sheet of €1,350bn and a book value of total equity of €64bn, a simple leverage of 21 times, but its market capitalisation at only €14bn tells the story in a more realistic way. No doubt, in a half-decent economy a bank in this position can fiddle along for a while, but Germany is turning sour, very sour. Germany’s economic prospects amount to a count-down to Deutsche Bank’s destruction, and Commerzbank’s with it.

The short-term consequences of the realisation that Lehman was a teddy-bears’ picnic compared with an approaching feast for grown-up grizzlies are expected to be a dash for dollar cash. That will be true in the US investment community, which according to FINRA in September had outstanding margin and cash loans of $556bn. For junk-rated corporations, as well as the medium and small companies that comprise eighty per cent of any modern economy, their bankers coming under pressure and concerned for their own bottom lines will rapidly withdraw lending facilities. Those that lose their banking facilities will defer payment to their suppliers while trying to get outstanding payments in earlier. Inventory will simply accumulate and there will be widespread bankruptcies.

Nearly eight out of ten US consumers are living pay-check to pay-check, as they are in the UK. The music in the non-financials, on Main Street, must play on and government must pay the piper. Other than subsidies and welfare there will be no cash. But the banks will be caught with non-performing loans, and governments will face both a collapse in tax revenue and an escalation in welfare commitments. We are approaching an end to the fiat monetary system: monetary inflation must accelerate at an even greater pace to keep the system from imploding.

The signal a crisis is in the wings comes from alternatives to state currencies and related financial assets. Initially, it is about preserving wealth with suitable stores of value and portfolio diversification to offset failing conventional investments. So far, the one accessible safe haven which has been in the headlines is gold, but there are other precious metals, particularly silver, and platinum. Palladium’s price is so distorted by shortages that any accumulation of it on monetary grounds is ill-considered.

Investors who think the scenario outlined above is a real danger will exchange increasingly worthless fiat for a precious metal. It is never too late. The lacklustre performances of silver and platinum so far, as well as the general disinterest in mines extracting all precious metals confirms that the current phase of gold’s bull market is only in the initial stage. The initial stage of any bull market is driven by a loss of bearish momentum combining with accumulation into the safe hands of insiders and knowledgeable investors. The insiders today are not the conspiracy theorists, they are always there. The insiders in precious metal markets are the professional operators who detect a change in the market; those who are usually short and needing to cover, the central bankers who privately detect a change in long-term monetary trends, and those who have experienced and understood previous cycles of credit.

For gold, this phase commenced with the end of the bear market in December 2015. The second bull phase, marked by the price break-out only five months ago, is only just getting under way. This is illustrated in Figure 1. Now professional investors can be expected to get on board, and their interest is likely to be reflected in increasing portfolio allocations in favour of gold ETFs and mining shares. If investing history and investor psychology are a guide, silver and platinum will find now buyers as well, as these investors look for lagging alternatives to gold. Therefore, their prices should begin to reflect the monetary considerations that are already apparent in gold’s performance.

According to Dow theory, which is the guiding light for all momentum investors, the third and final stage of a bull market still lies ahead and will see increasing public participation. For stockmarkets generally, it marks a final blow-off stage, with inexperienced investors being sucked into what must seem to them a sure-fire way of making money.

Before we arrive at that point, portfolio managers and other professional investors will continue to make the mistake of thinking gold, silver and platinum are simply investments. They are not. They are the sound alternative to unbacked government currency, and so long as they measure their performance figures in a fiat currency they are bound to persist in making this error.

Demand for precious metals in physical form, and their physicality must be stressed, is primarily a reflection of a desire not to hold state-issued currencies, and depending on how monetary policies evolve, their use as money could be threatened absolutely. That is for the future. Meanwhile, the market position indicates to those at the investment coalface who follow Dow theory that we are embarking on a second stage of a wider bull market in gold, and it is therefore time to get a market perspective not just on gold, but also the two principle metallic alternatives, silver and platinum.

We must now look at all three stores of value.

Gold

Gold always has been and remains a monetary metal, with central banks recorded as owning 34,408 tonnes in their monetary reserves, an increase of 4,406 tonnes since 2008. It is sound money, with no counterparty risk, so for central banks it is an insurance against monetary failure of other currencies and against systemic failure generally.

Assessments of above-ground gold stocks in an attempt to give us a post-fiat global quantity of sound money are always incorrect, partly because the true quantity of above-ground gold stocks is unknown, and because only gold held for monetary purposes are relevant.

Since 2009, the World Gold Council’s estimates, which are commonly quoted as gospel, have been based on estimates by Thompson Reuters GFMS (GFMS). By 2011, GFMS’s figures estimated the figure to be 171,300 tonnes, which included an estimate for above-ground stocks of 12,780 tonnes in 1492, the year Columbus, as Fats Waller memorably put it, sailed the ocean blue.

James Turk of Goldmoney with assistance from Dr Juan Castañeda examined the basis of GFMS’s estimate and concluded it was too high. The reasoning can be found in Turk’s paper, here (see pages 9-13 in particular). Instead, Turk’s estimate for the 1492 stock is 297 tonnes in accordance with other research, and his estimate of subsequent production before 2011 is 3,573 tonnes less than the GFMS calculation. By end-2018, working on subsequent estimates of annual figures for mine production[ii] (though there is some variance between sources) in my opinion the 2018 estimate published by the WGC at 193,472.4 tonnes is too high by 17,206 tonnes, nearly 10% above where it should be.

One may wonder why a 10% difference in above-ground stocks matters, but it does matter hugely when we consider the only other assessed figures which are known with a degree of confidence. Going on the WGC’s figures for bars and coins held for investment and which we are entitled to assume are based on reasonably solid estimates, and adding in monetary gold declared by central banks, we have a total for gold classified as money of 75,686.5 tonnes, which we must regard as the base figure for gold’s global money supply, not 193,472.4 tonnes as commonly supposed, or even our lower modified estimate of 176,266 tonnes. But given that on Turk’s figures and subsequent mine output estimates we are left with not 117,786 for non-monetary uses but 100,579 tonnes, future supply from scrap on rising prices will be significantly tighter than commonly thought.

This particularly matters in the context of the large quantities of gold substitutes in regulated and unregulated markets. Simply adding the three major markets, the London Bullion Market, Comex and the Shanghai gold futures, gives us the paper equivalent of 9,563, 1,485 tonnes and 552 tonnes respectively as at end-June 2018 (the last date for which BIS figures are available). To these amounts of paper gold must be added an unknown quantity of unallocated gold accounts at the bullion banks, which are fractionally reserved.

These numbers repfresent the establishment’s bear position.

If the move out of fiat money into gold develops, not only will the financial system have to fulfil demand for sellers of fiat for gold, but it will also have to absorb the liquidation of paper substitutes. In an orderly market which has time to adjust to rising prices, it is not necessarily a problem and paper substitutes can survive. But when the origin of the new demand stems from a systemic and monetary crisis, the price effect is likely to be sudden, threatening the whole bullion banking system.

Given the scale of the risks from an increasingly likely financial crisis, the relationship between gold and fiat money is now the most urgent consideration facing everyone owning or managing fiat-denominated financial assets. Only, very few of them know it.

Silver

When silver was the backbone of coinage, its purchasing power relative to gold for centuries was in the region of 12:1 before Sir Isaac Newton, when he was Master of the Royal Mint, fixed it at 15.5:1 early in the eighteenth century. The bimetallic standard he introduced was not a successful concept, because the preference for circulating money in the economy clashed with a trade settlement preference for gold among merchants. Eventually, the European countries on a silver or bimetallic standard moved to a gold only standard in 1873, though silver still circulated in coinage, and the price of silver relative to gold fell substantially.

Since then, silver has been predominantly an industrial metal in the West, but it still circulated in the Middle East and elsewhere in the form of Maria Theresa coins as late as the early-1970s. Today, the gold-silver ratio stands at 84, a far cry from Newton’s 15.5, and from the estimated rarity in the earth relative to gold of about 18.75 times.

According to the Silver Institute, total supply in 2018 was 1,004.3 million ounces, of which 855.7Moz was mine supply and 151.3Moz was scrap. Total physical demand (including 181.2Moz for coins and bars) was estimated slightly more at 1.033.5Moz. Additionally, net investment-related flows added a net 50.1moz demand to give a total deficit of 80.1moz, or 8% of total supply.[iii]

As a mining by-product, silver’s supply is strongly influenced by mine production of base metals, particularly lead, zinc, copper and gold. Primary silver mines only account for 26% of total mine output world-wide. Consequently, the ability of mines to increase silver output to meet rising demand is very limited. Furthermore, in an economic downturn the output of base metals is likely to decline due to falling demand, reducing the supply of silver as well.

Industrial demand at 57% of total supply has been remarkably stable in recent years but obviously can be expected to fall in an economic downturn, offset to a degree by low cyclicality in photovoltaic, electrical and electronics and growing disinfection markets. The balance between declining mine supply and declining industrial demand will also be determined by their relative rates of decline. 63% of total silver supply (including scrap) is tied to base metal demand, while industrial use absorbs only 57% of total supply. Therefore, a recession can be expected to have a broadly neutral effect on the overall industrial supply/demand balance.

Annual bar and coin sales at 181.2moz are only worth $3.2bn and should be viewed in the context of Asian investment demand, where silver coin has traditionally been accepted as circulating money. In the event of monetary disruption, the potential for silver demand in these populous markets is enormous. India has been an important market, with a history of high levels of imports, even in relatively stable times. Since the start of 2010, India has imported well over a billion ounces.[iv]

The history of demand in India shows it to be strongly associated with wealth preservation, and given the high gold/silver ratio, this can only fuel increasing Indian demand for silver when the gold price is rising. China has been India’s largest supplier, and rising markets are also likely to reduce any surplus silver China may have for export, putting a squeeze on Indian supplies.

As a producer, China ranks third as a mining nation, and is also a large consumer at 166Moz annually. Since 2014 investment demand for bars has been subdued in the wake of anti-corruption measures, a factor which has put negative pressure on global prices. Annual investment demand in China by 2017 had fallen to 7.5Moz, representing only 5% of the world total.

As monetary circumstances change and the price of gold rises, so should Chinese investment interest in silver. Demand is likely to come from ordinary savers in both jewellery form as well as for bar and coin. It is the money of the masses, but it must be admitted that sophisticated millennials are likely to consider cryptocurrency alternatives as well.

As a rule of thumb, when the price of gold rises, the price of silver tends to increase between 1.5-2.0 times that of gold. Furthermore, in the early stages of a bull market for gold, silver tends to lag, catching up later. This can be explained by financial markets regarding gold as more of a monetary metal than silver, turning mainly to gold when prospects for currency debasement initially appear to increase.

Gold’s bull phase commenced in December 2015 and was only confirmed when it broke out of a long consolidation last June. So far, the dollar price of gold has risen by 42%, while the silver price has risen just 26%. This is consistent with an early phase of a continuing bull market for precious metals and suggests that an acceleration in silver’s rising price will occur on gold’s next bullish move.

Platinum

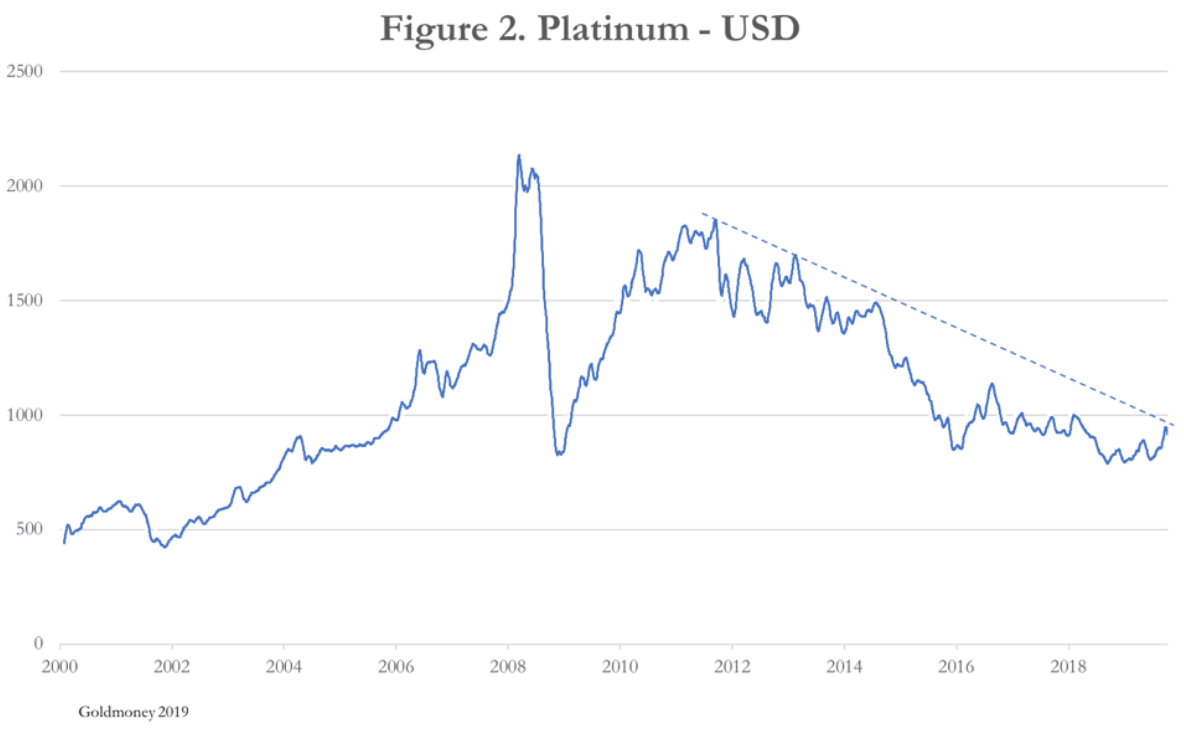

The chart for platinum in Figure 2 shows it has failed so far to convincingly exit the bear market that commenced in 2011 and today is only 15% higher than the lows recorded following both the Lehman shock and in August 2018. So long as these two lows hold, technical analysts will conclude a double bottom has been formed, in which case the platinum price has the potential to more than double.

Platinum is very rare, with only one thirtieth of gold’s occurrence. 72% of the annual production of about 190 tonnes comes from South African mines and 8% from Zimbabwe. When recycling is taken into account, total annual supply in 2018 was 8,060 million ounces, expected to rise to 8,390Moz in the current year.[v]

Platinum prices have suffered in recent years as falling demand-trends for diesel engines, which are more platinum dependent for catalytic conversion, have been replaced by rising demand-trends for petrol, which are more palladium and rhodium dependent. The result is that analysts forecast deficits of over 700,000 ounces for palladium in 2020, a trend likely to continue, while platinum continues to have a surplus of supply over industrial demand.

It had been expected that the motor industry would switch back to using platinum more in catalytic converters than the current palladium/rhodium mix. Despite the rise in palladium prices, there is little sign of this happening. Furthermore, the downturn in vehicle demand in China and elsewhere while emission regulations continue to tighten encourages analysts to reduce their forecasts for catalytic demand for platinum group metals overall.

Consequently, platinum demand has become increasingly dependent on investment. But here, a disappointing price performance has led to persistent ETF liquidation in recent years, though this appears to be changing. Jewellery demand has been broadly flat.

In short, the platinum market currently lacks obviously positive factors, but that is discounted in the disappointing price performance and the current price level. All that is required to drive prices higher is a boost to the investment case, when the price could easily double from that double bottom, outperforming gold perhaps on the next leg up. And that will probably be as a wider understanding of monetary debasement by investment managers and the general public develops, overwhelming the physical quantities available.

[i] See https://www.mckinsey.com/~/media/McKinsey/Industries/Financial%20Services/Our%20Insights/Global%20Banking%20Annual%20Review%202019%20The%20last%20pit%20stop%20Time%20for%20bold%20late%20cycle%20moves/McKinsey-Global-Banking-Annual-Review-2019.ashx

[ii] See https://www.statista.com/statistics/238414/global-gold-production-since-2005/

[iii] See https://www.silverinstitute.org/silver-supply-demand/

[iv] See page 2: https://www.silverinstitute.org/wp-content/uploads/2017/05/IndiaMarketStudySep2017.pdf

[v] See https://www.platinuminvestment.com/files/438549/WPIC_Platinum_Quarterly_Q2_2019.pdf

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.