Post-tariff considerations

May 16, 2019·Alasdair MacleodPresident Trump has declared he will extend tariffs of 25% on all America’s imports of Chinese goods. China is responding with tariff increases of its own. The consequences of this action and reaction will be to kick-start higher monetary inflation in America and an economic slump. This article explains how an overdue credit crisis will be made considerably worse by trade protectionism. It could become the credit crisis to end all credit crises and undermine the whole fiat currency system.

Introduction

Following President Trump’s imposition of 25% tariffs on all Chinese imports, it is time to assesses the consequences. Already, we have seen a contraction in US-China trade of 20% in the first three months of 2019 compared with the same quarter last year, and also compared with the average outturn for the whole of 2018.[i] This contraction was worse than that which followed the Lehman crisis.

In assessing the extent of the impact of Trump’s tariffs on the US economy, we must take into account a number of inter-related factors. Clearly, higher prices to US consumers will hit Chinese imports, which explains why they have dropped 20% so far, and why they will likely drop even more. Interestingly, US exports to China fell by the same percentage, though they are about one quarter of China’s exports to the US.

These inter-related factors are, but not limited to:

- The effect of the new tariff increases on trade volumes

- The effect on US consumer prices

- The effect on US production costs of tariffs on imported Chinese components

- The consequences of retaliatory action on US exports to China

- The recessionary impact of all the above on GDP

- The consequences for the US budget deficit, allowing for likely tariff income to the US Treasury.

These are only first-order effects in what becomes an iterative process, and will be accompanied and followed by:

- Reassessment of business plans in the light of market information

- A tendency for bank credit to contract as banks anticipate heightened lending risk

- Liquidation of financial assets held by banks as collateral

- Foreign liquidation of USD assets and deposits

- The government’s borrowing requirement increasing unexpectedly

- Bond yields rising to discount increasing price inflation

- Banks facing increasing difficulties and the re-emergence of systemic risk.

We can expect two stages. The first will be characterised by monetary expansion will little apparent effect on price inflation. Putting aside statistical manipulation of price indices, this is the current situation and has been since the Lehman crisis. It will be followed by a second phase, following an acceleration of currency debasement. It will be characterised by increasing price inflation, and ultimately the collapse of purchasing power for unbacked fiat currencies.

The trade framework

The simple accounting identity at national level linking trade with changes in the quantity of money and credit is comprised of three factors: the budget deficit, the trade deficit, and changes in total savings. They are captured in the following equation:

(Imports – Exports) = (Investment - Savings) + (Government Spending – Taxes)

In other words, a trade deficit is the net result of a shortfall in the combination of a savings surplus over industrial investment and the budget deficit. For a detailed explanation as to why this is so, see Trade wars – a catalyst for economic crisis. The equation tells us that it is the expansion of money and credit which gives rise to trade imbalances, which is why when there is no change in the savings rate and in the absence of other factors the twin deficits arise. Otherwise, monetary inflation would lead directly into price inflation, the effect in a closed economic system.

Mainstream economists often disagree with this point, having discarded Say’s law. Say’s law explains the division of labour. It maintains that we specialise in our own production to buy all the other things we require and desire, and money is just the intermediation between our production, consumption and deferred consumption (savings). It was the iron rule of pre-Keynesian classical economic theory and allowed no latitude for state-issued money that was inflated into the system. Keynes had to disprove it (he did not – his definition was deliberately misleading) in order to develop his inflationist theories and create an economic role for intervening governments. It was this fundamental error of post-Keynesian economics that has led to successive economic crises, despite the ability of ordinary economic actors to adapt to government interference.

Understand this, and it follows that money and credit not earned through production can only lead to the importation of products from exogenous sources, or alternatively, fuel a rise in prices to reflect the increased quantity of money circulating between consumers and domestic producers. Free trade, the ability to substitute lower-priced goods from abroad for domestic equivalents, reduces the price impact of monetary inflation. If it wasn’t for the availability of foreign substitutes, price inflation would be far higher, which is why tariffs on imported goods only serve to push up price inflation.

Unintended consequences

Obviously, being a tax on imports, tariffs benefit the Treasury’s finances; a fact which President Trump continually boasts about. To be precise, a 25% tariff on all Chinese imports in the remaining five months of the current fiscal year (based on the first quarter of 2019) can be expected to raise $45bn, which reduces the Office of Management’s budget deficit estimate of $1,092bn[ii] for fiscal 2019 to $1,047bn. The tax benefit is therefore relatively minor, and likely to be more than offset by the recessionary consequences of higher tariffs on government tax revenues and welfare costs. This article will go into more detail why this is so.

If for a moment we assume there will be a limited impact on consumer demand from increased tariffs, the effect on prices at the margin would be to drive them sharply higher for all consumer goods in the product categories where Chinese supply is a factor, with some spill-over into others. Price inflation would simply begin to escalate. But given the indebtedness of the average American consumer, the ability to pay higher prices is obviously restricted, suggesting that overall demand must suffer, not just for imported Chinese goods, but for domestically-produced goods as well. It is therefore likely there will be both an impact on price inflation and a fall in consumer demand.

Besides the effect on consumers, manufacturers relying on part-manufactured Chinese imports and processed commodities now face cost pressures from tariffs which they may or may not be able to pass on to consumers. The cost pressures on manufacturers are bound to lead to a reassessment of their business models. This will be communicated to their bankers as increased lending risk, and they in turn will almost certainly restrict credit availability. The credit cycle would then move rapidly into a contractionary phase as both businesses and their bankers take fright.

Anyone who has analysed post-war credit cycles will be familiar with these dynamics. We are probably not there yet, despite the warning shot from financial markets in the fourth quarter of 2018. For now, the initial softening of consumer demand has led to a general assumption that monetary policy will ease sufficiently to prevent little more than a mild recession, benefiting capital values. Government bond yields have eased, and arbitrage across bond markets has ensured investment grade corporate bond yields have declined as well. Since end-November when the central banks began to ease monetary policy, the effective yield on investment grade corporate bonds, reported by Bank of America Merrill Lynch, has fallen from 4.8% to 4%. This is hardly an assessment of increasing lending risk.

As well as bond markets, equity markets are also expecting monetary easing, instead of a gathering crisis, and have rallied along with bonds. Clearly, financial markets have not noted the seriousness of trade protectionism, having become complacent while trade restrictions have generally eased in recent decades. However, market historians will note that this brief recovery phase was also the pattern in stock markets between October 1929, when the Smoot-Hawley Tariff Act was passed by Congress, and April 1930, two months before President Hoover signed it into law. If the correlation with that period continues, equities could be in for a substantial fall (in 1929-32 it was 88% top to bottom).

In the Wall Street Crash, equities fell as collateral was liquidated into falling markets. Non-financial assets, such as property, similarly lost value and productive assets (plant, machinery etc.) failed to generate anticipated cash flows. This nightmare was famously described by Irving Fisher, and has continued to frighten economists ever since.

While debt was a problem in 1929, it was generally confined to corporate borrowers and speculators. Today’s context of Fisher’s nightmare is in record levels of government, corporate and consumer debt. The potential disruption from the unwinding of the credit cycle is therefore worse today. Trump’s trade protectionism so far is targeted at one country, unlike Smoot-Hawley which was across the board. At first glance, Smoot Hawley was more dangerous, but it is the lethal combination of tariffs and the end of the expansionary phase of the credit cycle which should concern us.

The credit cycle with its periodic crises is both a given and overdue. The addition of trade tariffs will act as a catalyst to make things worse. Inflation and unemployment will rise, and as unemployment rises, government welfare costs will too. Being mandated, it will be impossible for the US Government to reduce them without revising the law. We can only guess the effect on the borrowing requirement, but with the Office of Management’s forecast deficit for fiscal 2019 at $1,095bn, perhaps over $1,200bn might be closer to the mark. The full impact is likely to be felt in 2020, when it could top $1500bn.

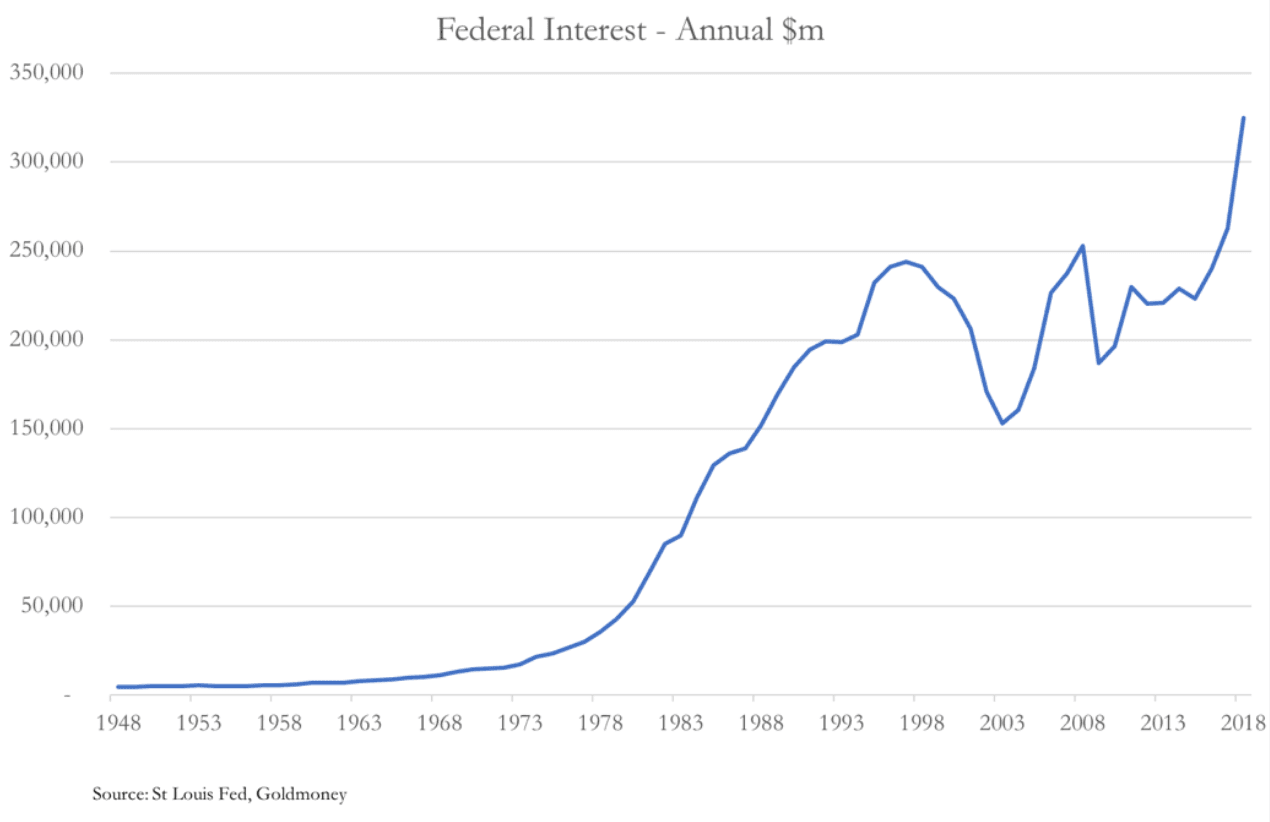

The cost of borrowing will escalate

With government borrowing already escalating, the interest rate burden on the government will become a very public issue. The following chart becomes the baseline for the government’s future borrowing costs.

Interest costs are already running away, before the addition of two other factors; a more rapidly accelerating borrowing requirement (as discussed above) and higher interest rates. After an initial round of monetary easing, higher interest rates can be expected to arise from a combination of three further factors. The most obvious is the increased rate paid by a borrower placing ever-greater demands on the bond market as the recession deepens.

With a gathering US and therefore global slump developing, foreigners will also become sellers of dollars and US Treasuries, simply because they do not need and cannot afford to run substantial dollar balances and investments. A foreign corporation may not like its home currency compared with the mighty dollar, but when costs and losses at its operating base need covering it has no option but to sell its dollars. Foreigners selling dollars and US Treasuries put all the funding onus on US residents, in conditions which, thanks to tariffs, are leading to increasing prices.

The impact of rising price inflation is bound to lead to higher nominal interest rates. While domestic investors can be expected to buy US Treasuries at supressed yields while recessionary fears persist, their appetite for guaranteed losses will be strictly limited. Commentators who have foreseen this difficulty expect quantitative easing to be reintroduced to guarantee affordable funding for the government. The argument in favour of more QE accords with the likely monetary response to collapsing consumer demand. It resolvs both the capital needs of hard-pressed banks and government funding demands.

Therefore, ahead of the next credit crisis, QE is the logical planners solution to stabilising an economy. It worked in the wake of the Lehman crisis. The inflationists are ready to try it again. Attention is even being paid to modern monetary theorists, the ultimate inflationists, who argue that increased government spending, so long as it is not inflationary at the price level, is good for the economy. It is the inflation assumption that could unwind it all.

Inflation will become the most important issue

Inflation is a more complex issue than presented by modern monetary theorists and other post-Keynesians. The root of price inflation is found in a combination of monetary inflation and the public’s changing preferences for holding money. An increase in the money quantity can be neutralised by an increase in the public’s preference for holding money relative to goods. Equally, if the public rejects money as a medium of exchange entirely, whatever the quantity, its purchasing power will vanish.

Modern economists take the view that monetary inflation does not appear to be a problem, citing Japan’s relationship between monetary expansion and prices. It appears that monetary expansion has not led to expected price inflation in the US, but here there is an issue with the statistics under-recording the price effect. Very few economists pay attention to relative preferences between money and goods.

In a credit crisis, it should be obvious that these preferences will change. Foreigners will reduce their relative preferences for dollars and will be a source of dollar liquidation to be absorbed by domestic US financial and non-financial sectors. A lower dollar in terms of its purchasing power of commodities will be the consequence.

For US residents the situation is more complex. Initially, banks will try to reduce outstanding credit obligations to the private sector, leading to deflationary pressures. Lending for working capital will be curtailed, and cash will also be raised from asset sales. Instead, banks will be buyers of US Treasury bills and short-maturity Treasuries. The Fed will reduce interest rates to zero again, and possibly even introduce negative rates in an attempt to counter credit deflation and reduce the cost of the government’s funding.

As mentioned above, the government’s budget deficit will increase due to a combination of falling tax revenue and increasing welfare costs. Initially, funding the deficit will not be a problem because banks will be keen to avoid private sector credit risk. Furthermore, the Fed will want to reintroduce QE as part of a stimulus package. With an embarrassment of funding options, government spending will escalate even more, justified as a fiscal stimulus by the inflationists. The scene will then be set for a second stage, where the banks, underwritten by the Fed, start expanding credit again in favour of the government.

Unfortunately, a weakening dollar combined with trade protectionism is likely to push up consumer prices, despite falling demand. It is not only foreigners who are overweight in dollars, but domestic holders are as well, which will become an issue when the credit crisis threatens the banks. Despite the banks’ efforts to de-gear their lending to businesses and individuals, a systemic crisis in a fractional reserve system cannot be avoided. Whether it starts in America or elsewhere (such as in the fragile Eurosystem) is immaterial. The only solution for the authorities, of course, is to chuck yet more money at the problem. They will have no alternative to accelerating the debasement of the currency to protect the banks.

The budget deficit widens even further

A broken economy with a collapsing currency forces a government to increasingly rely on monetary inflation as its principal source of revenue. The gap between a government’s spending and tax revenues widens even further. This returns us to the accounting identity described towards the beginning of this article: in the absence of savings, a budget deficit leads to a trade deficit.

With the budget deficit widening, so will be the tendency for the trade deficit. But we are now in a world where politicians feel they have no option but to discourage imports with even more trade protectionism. It is easier to tell the public that nasty foreigners are profiting from their economic misery than admit the fault lies squarely on the shoulders of the government’s excess spending.

The consequences for other fiat currencies

With the dollar being the world’s reserve currency, rising dollar interest rates and price inflation will affect almost all the other fiat currencies. We can argue over the fundamentals for various currencies, but what truly matters is which foreign currencies everyone owns. It should be noted at the outset that Americans own very little foreign currency liquidity, their currency being the reserve currency, and also because the dollar’s recent strength has reflected liquid inward flows.

It will be foreigners liquidating their excess dollars who call the shots. It is a myth that foreigners are short of dollars, perpetuated by those who seem to think that foreign loan obligations need cover for repayment. They don’t, and many of them will not be repaid anyway. More pressing is the problem of contracting global trade, requiring lower dollar balances and the liquidation of portfolio assets which will be falling in price, reflecting the slump. Call it the “Great Unwinding”, reflecting decades of inward investment since the end of Bretton Woods.

The combination of trade protectionism and the turning of the credit cycle threatens to result in an economic slump of severe proportions. The experience of Smoot-Hawley in the 1930s was that America’s trade protectionism rapidly led to a worldwide depression. Since the dollar was on a gold standard, commodity and food prices fell heavily. This time, with no gold backing, it will be currencies that lose purchasing power, at least to the extent they neutralise contracting demand, that being de facto monetary policy already. Therefore, there could be for a short time the appearance of price stability in other currencies, giving central banks the leeway to maintain their price inflation targets.

This will simply encourage central banks to run the loosest possible monetary policies, hoping for a controlled devaluation to stimulate demand. For a time, the only evidence of the true effect of these policies will not be rising commodity prices, but a rising gold price. Gold will be reflecting what is truly happening to prices while the balancing act between falling demand and fiat devaluation plays out.

The monetary planners will give themselves firepower to manage currencies through enhanced swap arrangements, and whatever other means they cook up. But it will always be inflationary. Consequently, they will lose control over prices, and will resort to other more direct means, such as price controls. It always happens that way, and they only hasten the end.

[i] See https://www.census.gov/foreign-trade/balance/c5700.html

[ii] Budget of the US Government Fiscal Year 2020, Table S-1 (page 107)

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.