Eliminating cash will also eliminate the checks and balances on banking policy and practice

Feb 22, 2016·Stefan WielerEliminating cash will also eliminate the checks and balances on banking policy and practice

The rhetoric against cash (bank notes and coins) has intensified over the past months. Academics and central bankers are advocating the elimination of large denominations of currency notes; some suggest to eliminate cash altogether. This hasn’t gone unnoticed by the public as the spike in Google Trends for topics such as “war on cash” shows. Now it seems the ECB is considering the first step towards implementation by eliminating the largest euro-denominated bank note: the 500 EUR bill. This bill, so described by ECB president Mario Draghi, “is being viewed increasingly as an instrument for illegal activities.”

We examine this trend and the recent rhetoric around the ‘war on cash’. We find the academic-led strategy to rush through a ban on large bills quite concerning; their analysis lacks thoroughness in examining those baring the costs of such a policy, while at the same time containing a high degree of misdirecting-spin by focusing on criminal activity rather than their underlying economic goals. We also discuss the following insights and findings, largely underreported thus far:

1. While most advocates for phasing out large bills are not getting tired emphasizing that smaller bills would not be affected, we show that the largest bills of each currency account for over 2/3 of all bank notes in circulation. Hence, many of the problems we think will emerge with a complete phase-out of cash would in our view already materialize by eliminating the largest bills.

2. One important finding we present is the systematically important use of large-denomination cash bills in times of market volatility. Eliminating the ability of savers to redeem cash and store it outside of the banking system would remove important checks and balances on commercial banks’ activities.

3. Removing the lower boundaries for central bank interest rate policy by phasing out cash would remove important checks and balances on central bank policy itself, something that historically has been associated with severe monetary instability.

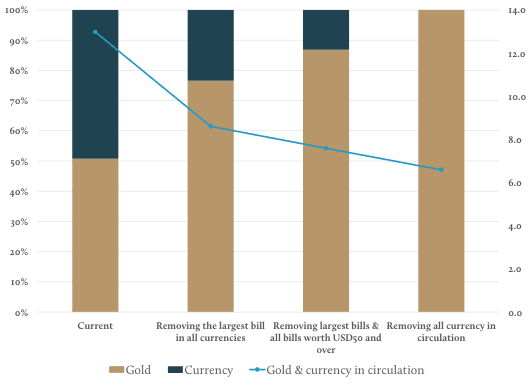

Our sister company BitGold has revolutionized the way people can save and spend in gold. As the cash phase-out advances, the appeal to hold gold as a savings asset without banking risk will only increase. We show the significance of large bills as a portion of physical currency and show that by removing them, the total value of gold would outweigh currency as a percentage of total physical money by 3:1.

By phasing out the largest bills, gold outweighs currency as percentage of total physical money by 3:1 from currently 1:1

Source: GoldMoney Research

View the entire Research Piece as a PDF here...

Eliminating cash will also eliminate the checks and balances on banking policy and practice

Avid readers of financial news have witnessed a sharp increase in rhetoric towards a phase-out of cash over the past months. Many countries, particularly Europeans, have already introduced upper limits on cash purchases in recent years. But more recently, we saw a push from academics and central bank officials around the world advocating the phase out of large bills or even an outright ban on cash.

The principal argument is that large bank notes are apparently mainly used in the underground economy, facilitating illegal activities such as the widespread drug trade and terrorism. Even those who make no pretense of their true intension for a cash phase-out, such as Harvard Economist Kenneth Rogoff1, claim that “Paper currency facilitates making transactions anonymous, helping conceal activities from the government in a way that might help agents avoid laws, regulations and taxes,” and use this as the main argument for a phase-out of large bills.

The latest development in this regard is the likely elimination of the EUR 500 note by the European Central Bank (ECB). Indications that the ECB is considering this step began to surface in early February. But the German Handelsblatt newspaper reported on Monday (March 15, 2016) that the ECB council has already decided to phase out the largest EUR note and has given itself 2 months to evaluate ways to implement this step. When ECB president Mario Draghi spoke in front of the European Parliament the same day he said that “There is a pervasive and increasing conviction in world public opinion that high-denomination bank notes are used for criminal purposes,” but he did not confirm that the phase out of the note is a done deal according to Bloomberg News.

Moving to a cashless society has been a topic in academia for a while now. The strict opponents of such a policy have dubbed it “the war on cash”. However, the general public has not really caught on this until very recently when evidence that central banks are increasingly pushing into this direction has become more and more obvious. Google searches for “war on cash” spiked sharply in February, in tandem with similar searches in other languages such as “Bargeldverbot” in German (see Figure 1).

Figure 1: There has been a sharp rise in google searches related to the phase-out of cash as of late

Source: Google Trend, GoldMoney Research

Central bank officials such as Mario Draghi insist that there is no war on cash and that the phase out of large bills is to serve fighting criminal activity which allegedly flourishes due to existence of large bank notes. According to Mr. Draghi, smaller bills would not be touched. Critics of a cash phase-out say that the elimination of large bills is only first step and that ultimately all bank notes and coins will disappear. However, we find that most of the problems that come with a total phase-out of cash will already materialize when just the largest bills are taken out of circulation.

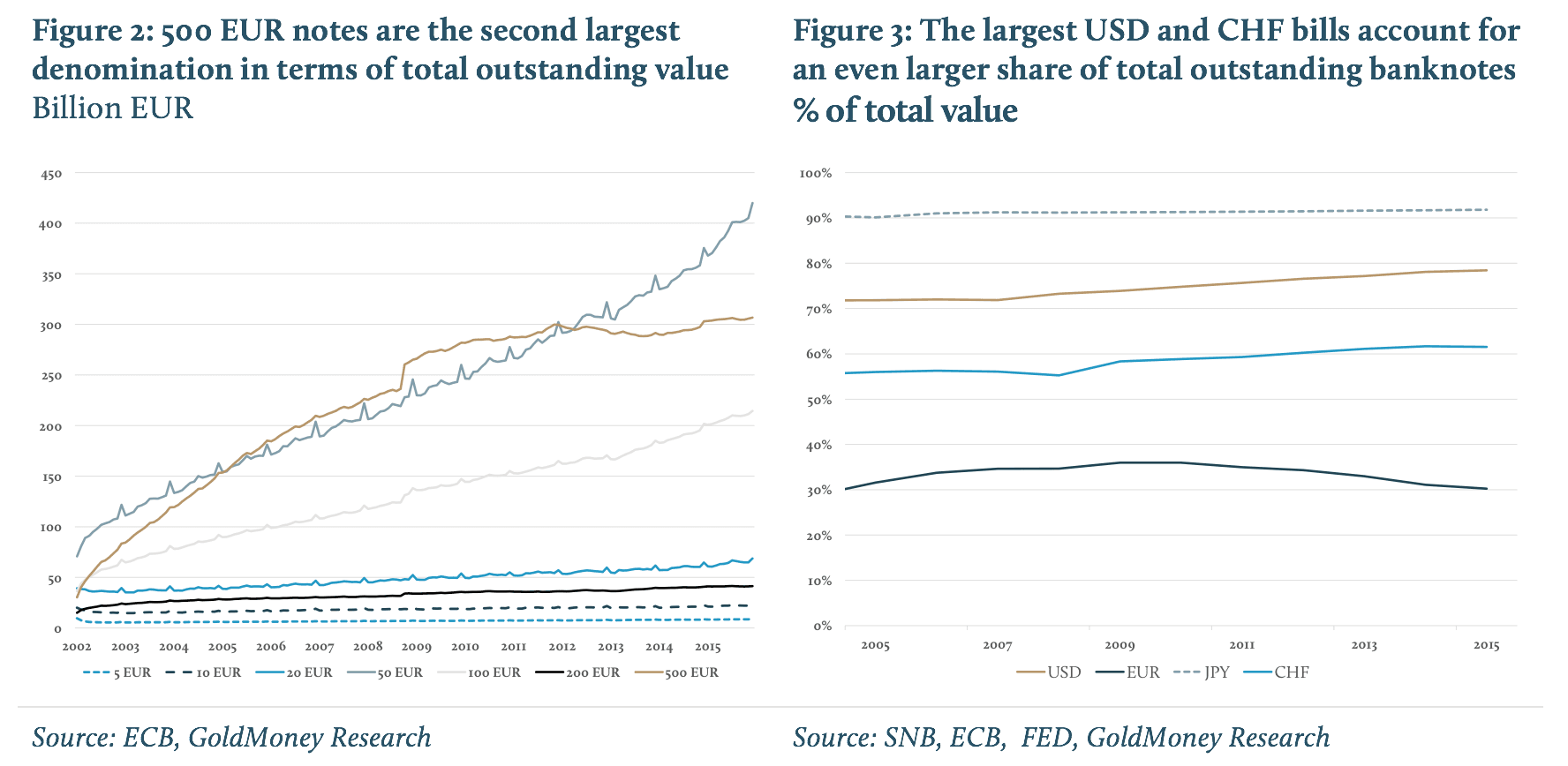

The 500 EUR note accounts for nearly 30% of all outstanding EUR bills. And the EUR is rather the exception when it comes to the breakdown of bank notes by denomination. The 100 USD bill for example, the largest US bank note in circulation in the current series, accounts for 78% of all outstanding bank notes. And all 10’000 YEN notes account for 92% of all outstanding YEN bank notes.

We collected data on bank notes and coins in circulation for the 11 most traded currencies in the world plus the Indian Rupee, Brazilian Real and the Russian Ruble. The countries issuing these currencies account for about 77% of global GDP. Combined, all the currency in circulation is about USD5.2tn at current exchange rates. Importantly, the largest bills account for about USD3.6tn, or close to 70%. Hence, extrapolated to the entire world, there is about USD6.39tn worth of currency in circulation. Removing just the largest bills of all currencies, we estimate that USD4.4tn worth of currency would disappear.

By way of comparison, according to a report by GoldMoney founder James Turk, the combined above ground stocks of gold were roughly 155 thousand tons by the end of 2011. Including the 12 thousand tons that have been mined since means that total above ground gold stocks are priced at roughly USD6.6tn which brings the current ratio of currency in circulation to gold to around 1:1. However, eliminating just the largest bills would bring the ratio to 3:1.

Table 1: The largest bills in circulation account for over 2/3 of all currency in circulation - End of 2015 where available

Source: GoldMoney Research, Bloomberg, FED, ECB, BOJ, BOE, RBA, SNB, BOC, BM, RBNZ, SRB, RBI, BCB, CBR, IMF

In Keynesian economics, saving cash, either on a bank account of simply by accumulating bank notes is labeled as hoarding in order to give it the air of something nefarious. However, saving for a child’s college education can hardly be regarded as an anti-social thing, and the same goes for saving for a house or simply for bad times, or for all manner of sensible financial planning. Rather than speculating in assets such as stocks that exhibit volatile prices, people naturally tend to have at least part of their savings in cash in order to reduce risk. Cash savings can either be on a bank account or it can be in physical cash. In this context, large bills have helped savers in times of increased risks in the banking sector. For example, the issuance of EUR 500 bills spiked sharply in 2009, at the height of the credit crisis. It coincided with a spike in the TED spread - the difference between the interest rates on interbank loans and US Treasury-bills – which reflected the rapid loss in confidence in commercial banks (see Figure 3). Hence, large-denomination cash bills have helped savers to reduce their counterparty risk in times of market volatility (see Figure 4)

This is important. Having the ability to withdraw cash from is an important element in the checks and balances on banks. Banking regulation is there to protect savers by imposing limits on what banks can do with their clients’ money. But if savers lose confidence in the banks, or in the regulators thereof, something that has become far more common post-2008, the only thing they can do to protect themselves is not to lend money to a bank as deposits. One can argue that even in a world without cash, savers have the ability to move their savings from a bank they don’t trust to another. But what if there is not one bank they can trust, say if they lose trust in the regulatory regime? Eliminating the ability of savers to withdraw cash from a bank could create increased moral hazard among banks. After all, if they all act the same, there would be no risk for a bank run anymore because there is no place to hide for savers. The sorts of banking practices that contributed to the 2008-09 global financial crisis would become all the more likely were cash to be banned outright.

Clearly, one of the aims for scraping large bills could therefore be to limit the ability of savers to withdraw cash in times of crisis. While this might help to protect balance sheets of commercial banks, this comes at the expense of savers, who, for better or worse, have to assume the default risk of at least one institution.

But the elimination of cash would not just remove important checks and balances on commercial banks. Another potential motive for a complete cash phase-out has become even more obvious over recent months. Since the 2008/2009 financial crisis, central banks around the world have held interest rates at historical lows. The US Federal reserve has held the FED lending rate near zero for nearly 7 years. Other banks have followed, and some didn’t stop there. After central banks of some smaller economies such as Switzerland have introduced negative interest rates earlier, Japan and the ECB have recently followed suit. The hope was that this would encourage spending which in turn would bring back economic growth. However, the much desired effect in consumption and thus economic growth has so far not materialized. Interestingly, while institutional investors in countries with negative interest rates effectively pay to lend their money to banks or the government already – a big problem for pension funds – savers have so far been spared negative rates on their savings account. For example, we know of only once Swiss bank that has decided to pass on negative rates to its clients. Hence NIRP and ZIRP had so far mainly one effect, to drive up asset prices as large institutional investors have been forced to chase the same assets the central banks were also buying. But in order to generate the desired effect on consumption, negative interest rates will ultimately have to be passed on to savers. And there is where the problem lies. Savers might not be willing to either simply spend their savings away in order to avoid paying somebody to lend their money to. As the push for negative interest rates intensifies, central banks face the dilemma that savers might simply opt to pull their money out of banks altogether and store cash at home or in a safe. Not just would this undermine all efforts by central banks to stimulate growth with negative rates, it would also affect aggregate bank deposits. At the moment, the ability to simply store cash currently sets a lower boundary for how far central banks can push rates lower. Eliminating large notes would complicate that. Eliminating cash entirely would make it impossible. A phase out of cash, and be it just the largest bills, would effectively remove this checks and balances on central banks as well. It is therefore obvious that central banks are not honest with their constituents of why they push for a cashless society.

In the end it’s the savers who will pay the price. Based on our estimates for the largest bills in circulation, at 1% average negative rates, savers would be exposed to an additional USD44bn p.a. in additional costs just from not being able to hold cash (see Table 2, next page). If all currency in circulation would be eliminated, this jumps to USD64bn. At -5% interest rates, these numbers increase to USD219bn and USD320bn p.a., respectively. To be clear, this is not the total amount of negative interest rate costs savers face, those are a lot higher as at this point, cash accounts only for a small portion of all savings. It is simply the costs that they could have otherwise avoided by moving some of their savings into cash. That cash would then be no longer available. But the problem lies beyond costs as it removes the lower boundaries for central bank policy and would allow central banks to enter unchartered territory.

However, just as ZIRP has not led to desired effect and to a lot of unwanted side-effects such as soaring assets prices, NIRP might achieve the same, even if cash is abandoned. Faced by two choices, either spend their savings even though they don’t want to or pay a penalty for lending money to banks, people might simply do the same things institutional investors such as pension funds have done for a while now. Instead of spending their money, they might buy assets instead which would further drive up the price of real estate and other real assets. And there is another obvious choice. Gold has been the money of choice for 1000’s of years. The value of the total above ground stocks of gold and the value of all currency in circulation is currently about the same. Removing the largest bills from the equation would mean that gold would have to assume a much larger role going forward. Our sister company BitGold has revolutionized the way people can save and spend in gold. With BitGold, savers can hold a cash-like asset without storage costs, negative rate related fees (direct or indirect), but engage in payments and digital commerce easier than cash. As the cash phase-out advances, the appeal to hold gold as a savings asset without banking risk will only increase.

Table 2: Eliminating the largest bills in circulation would have severe negative impact for savers in a negative interest rate environment

End of 2015 where available

Source: GoldMoney Research, Bloomberg, FED, ECB, BOJ, BOE, RBA, SNB, BOC, BM, RBNZ, SRB, RBI, BCB, CBR, IMF

View the entire Research Piece as a PDF here...

1. Rogoff, Kenneth: "Costs and benefits to phasing out paper currency", Harvard University, May 16, 2014.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of GoldMoney, unless expressly stated. The article is for general information purposes only and does not constitute either GoldMoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, GoldMoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. GoldMoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.