Dollar FMQ update

Apr 21, 2016·Alasdair Macleod

The Fiat Money Quantity continues to rise at an accelerated pace, and now stands at $14.286 trillion.

If it had continued to rise at the pre-Lehman crisis pace, it would be standing at only $8.474 trillion, a difference of $5.82 trillion. FMQ measures the quantity of money issued in return for the gold, first deposited in the forerunners to today’s commercial banks, and then transferred to the Fed after the creation of the Federal Reserve system. It is the sum of true money supply and the bank’s reserves held on the Fed’s balance sheet, adjusted for short-term distortions applied to the reserve total, particularly, but not limited to, repurchase and reverse-repurchase agreements.

FMQ should not be confused with conventional money supply measures, which record money in public circulation only. Its purpose is to quantify the distance of travel between sound and unsound money.

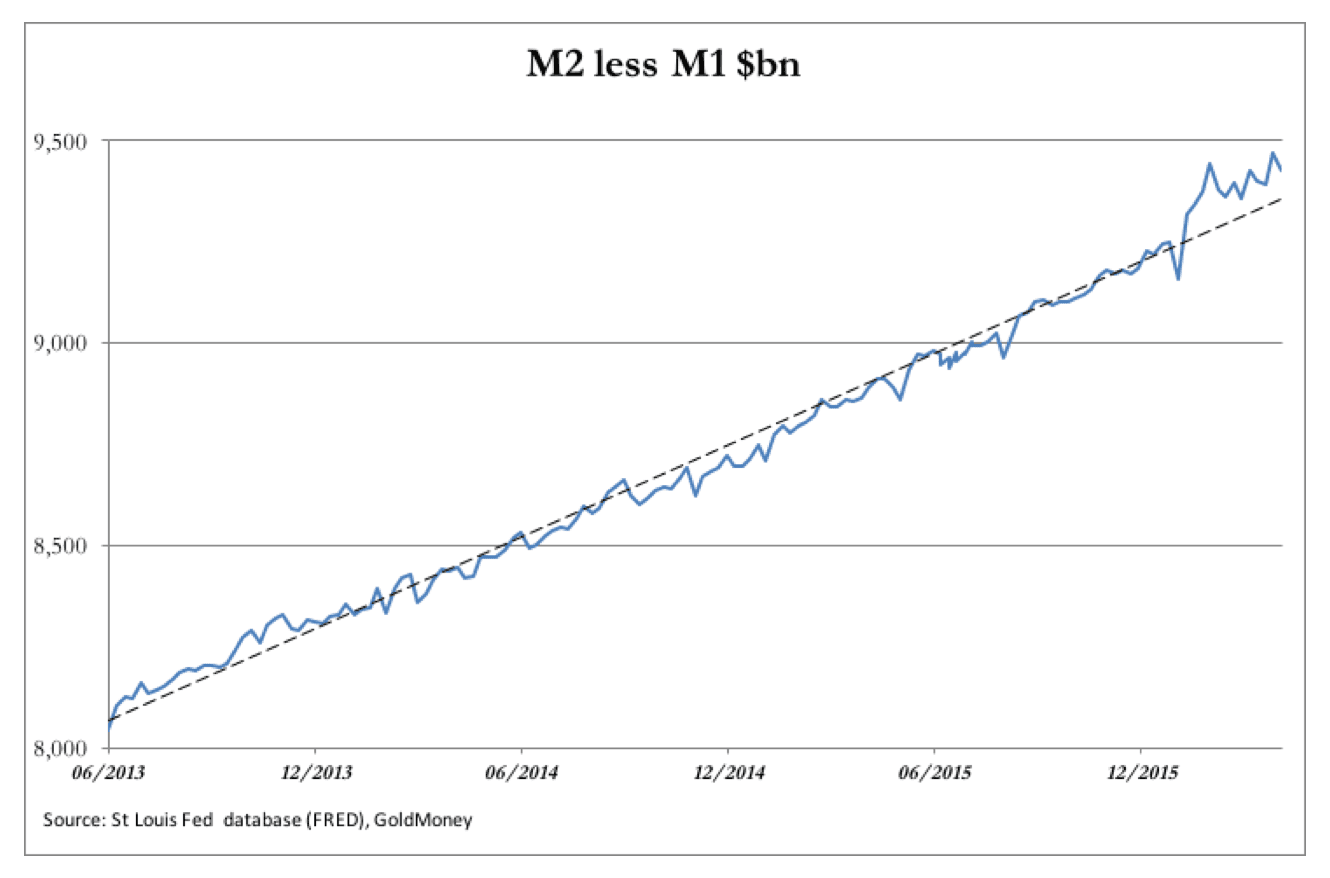

February’s increase was $166bn, a significant jump after a stagnant second half of 2015. We shall see if this is the start of a new acceleration. If so, it will be reflected in checking accounts, savings deposits, bank reserves at the Fed, reverse repos or any combination thereof. The recent trend before March had seen little or no growth in bank reserves, and an increase in checking and saving account balances. This is reflected in the difference between M2 and M1 money supply figures, which is the next chart.

The difference between these two measures of money supply approximates to bank lending. And here it can be seen that bank lending has increased above trend since early January. The cause for this move away from a remarkably tight correlation to the trend is potentially alarming, given a stagnating economic background. Without a noticeable increase in economic activity, increased bank lending can only be associated with lending for financial speculation, or for prolonging the life of distressed businesses.

The big jump in bank lending occurred when the S&P500 Index fell sharply in January, so it was not associated with increased financial speculation. However, at the quarter-end, there would have been financial difficulties emerging in the shale oil industry, and probably elsewhere, requiring loan extensions.

It would therefore appear that this increase in bank lending indicates financial difficulties in the non-financial sector.

Interest rates

On superficial analysis, the tendency for bank reserves at the Fed to stabilise, together with the increase in bank lending, suggests that the Fed should raise interest rates to control the pace of credit inflation. Alternatively, if this increase in bank credit is a reflection of debt distress, rate rises might be best deferred, and even negative interest rates considered. It is no wonder that the Fed initially called for gradually increasing rates, and then put the planned rate rises on hold.

From the Fed’s viewpoint, there is a potential nightmare unfolding, of which it is surely aware. Even if the increase in bad debts is confined to the energy sector, the recovery in the oil price is not yet sufficient to reduce the threat of widespread failures, compromising the capital of commercial banks. However, if the oil price rises much further it might take the financial pressure off shale oil producers. But if that happened, it would likely be accompanied by a significant rise in other raw material prices as well, pushing up price inflation later this year, potentially well above the Fed’s 2% target. Put another way, measured in a basket of commodities the dollar can be expected to weaken significantly in the absence of sufficiently aggressive interest rate rises.

On this analysis, rates should be raised sooner rather than later to discourage latent price inflation. But all surveys and anecdotal evidence point to a stagnating economy that requires monetary stimulus instead, if conventional macroeconomic policy were to be applied. It looks like a condition of developing stagflation, and we know how that ended in the 1970s. What makes it even more difficult for central bankers setting rates is that in modern macroeconomics, no sound explanation for stagflation exists. And if you don’t understand why a condition exists, how can you successfully formulate a policy response?

A better understanding of price theory is obviously required, but Fed economists instead will simply claim we are in uncharted waters. Today’s problems are a by-blow of the Fed’s earlier monetary policies, which along with the other major central banks, have been implemented to stop markets from properly assessing risk and clearing at realistic prices.

Instead of enquiring where it has all gone wrong, the Fed would rather take comfort from the US Government’s engineered statistics, particularly the lack of price inflation recorded by the CPI, despite the expansion of monetary aggregates since the financial crisis. The Fed seems likely to opt for the hope that interest rate rises can be continually deferred in the absence of recorded price inflation, and bad debts covered up by monetary policy for a while longer.

Implications for the gold price

As already stated, the purpose of FMQ is to quantify the distance of travel between sound money, which is gold, and unsound money, which is fiat currency and bank credit combined. FMQ can show the points at which the relationship between gold and fiat became too stretched in the past. The chart below shows the relationship between the nominal gold price and the price adjusted over time by both the increase in FMQ and above-ground stocks of gold.

In March, gold measured in 1934 dollars, and adjusted for above-ground gold stocks at that time, was the equivalent of $12.93. In other words, despite the increased risk of a collapse in the dollar’s purchasing power, in real terms gold is priced at about one third of the level President Roosevelt set in 1934. Therefore, on any monetary measure, gold is extremely cheap, and is back at the levels set in July 1976, and in 1999-2002.

This sort of historical perspective is useful, putting the first quarter rise in the gold price of only 20% in context. We should also note that China appears to be wresting control of the gold market from the US and London, since it now controls the physical market. Furthermore, by pricing physical gold in yuan at a twice-daily fix, China will be able to direct physical flows through Shanghai, instead of dealing in London and New York.

Perhaps, by moving pricing away from a dollar monopoly, gold’s enduring undervaluation is about to come to an end.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of GoldMoney, unless expressly stated. The article is for general information purposes only and does not constitute either GoldMoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, GoldMoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. GoldMoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.