Market Report: Quarter-end knockdown

Oct 1, 2021·Alasdair Macleod

This week saw a high degree of price capitulation as bullion banks used the dollar’s strength and a rally in bond yields to mount a bear raid on gold and silver. On Wednesday, silver traded as low as $21.45, down over 20% on the year, before rallying off these lows to trade at $22.19 in European morning trade today, down a net ten cents from last Friday’s close. After hitting a low of $1722, gold was marginally up by $4 at $1754 on the same time scale.

On the selloff, gold’s volume was high, aided by reports that China will import gas for electricity generation at any price to end crippling power cuts, driving WTI oil futures over $75. They have eased back a little overnight, but the message is clear: as we enter the northern hemisphere winter, global energy shortages and higher prices will be our fare. But for gold and silver, probably the real reason behind the bear raid was to get prices as low as possible for quarter-end book-keeping.

Comex saw high levels of deliveries yesterday: 1,146,800 ounces of gold (35.67 tonnes) and 7,585,000 ounces of silver (236 tonnes). These contracts have moved from being rarely stood for delivery to a means of obtaining bullion, with 14,688,700 ounces of gold (457 tonnes) delivered so far this year. The figure for silver is doubly impressive at 221,005,000 ounces (6,874 tonnes).

Ahead of the UK’s Basel 3 implementation deadline, the bullion banks are obviously desperate to close their short positions. But high Comex trading volumes and falling open interest on price weakness are only compatible with spread positions being closed, and not the shorts.

We tend to look at Comex statistics because the far larger London OTC forward market is opaque. All we know is that at the end of 2020, there were total forward and swap gold contracts recorded at $530bn, or 8,676 paper tonnes. While some of these positions will be between banks and can be closed out by mutual agreement a large and undefined amount is short to unallocated customer deposits. There is bound to be a move to reduce and close these positions to comply with Basel 3’s net stable funding ratio, which applies from 2 January — only three months away. This is likely to lead to far higher demand for physical gold and silver.

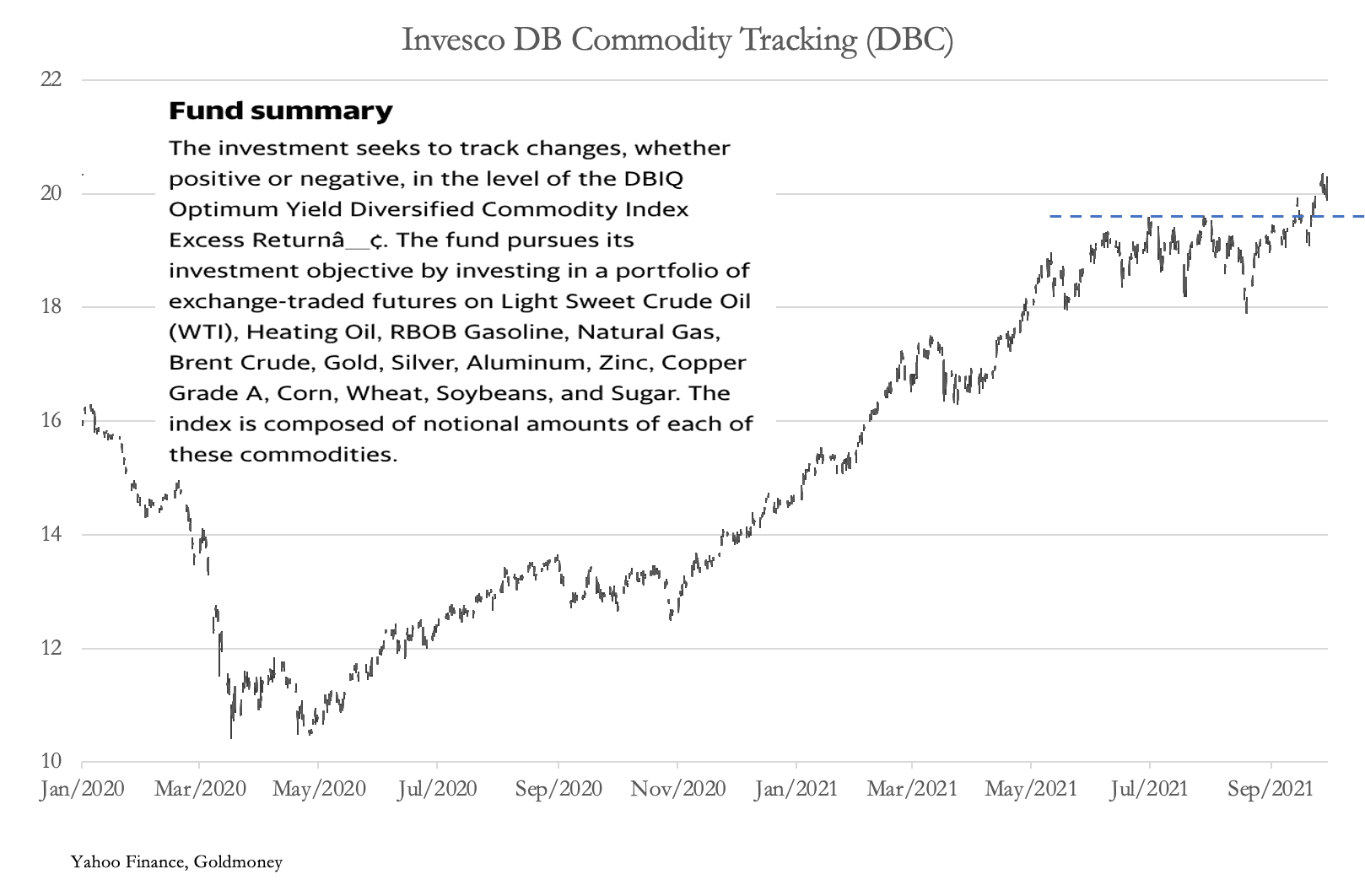

Gold and silver’s performance is sharply at odds with the commodity and energy complex, which driven by energy prices is trading higher, as our next chart, of Invesco’s commodity tracking ETF shows.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.